by Sam Kelly DipPFS, EFA, BA (Hons)

Managing Partner

Chorus Financial

Often the first question asked by clients considering an investment or pension with Chorus Financial! So, I thought this would be a good time to really dig into that, because for me, discussing the risks and potential downsides of an investment is as important as selling the benefits.

All investments carry some degree of risk, so the most critical element is that the investment is suitable for the client’s circumstances and falls within their personal risk tolerance. You will generally be asked for complete a risk profile questionnaire when seeing a financial adviser, and this will result in you being asked to confirm a level of risk, for example, low/cautious, medium/balanced etc. From there you would expect your financial adviser to build you a personalised portfolio appropriate to that agreed risk level.

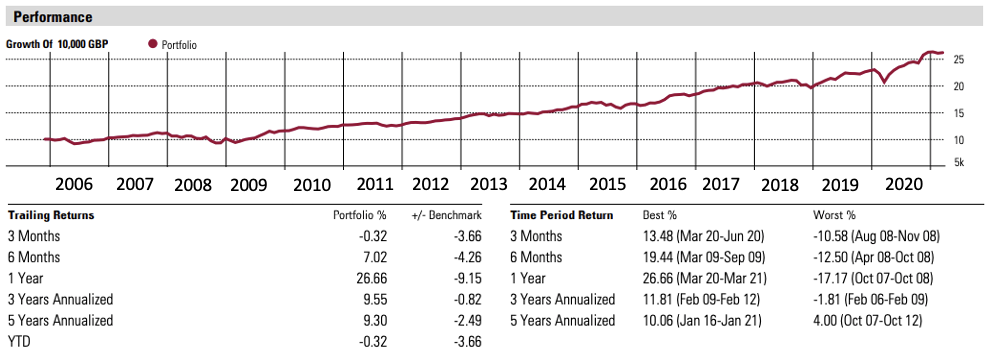

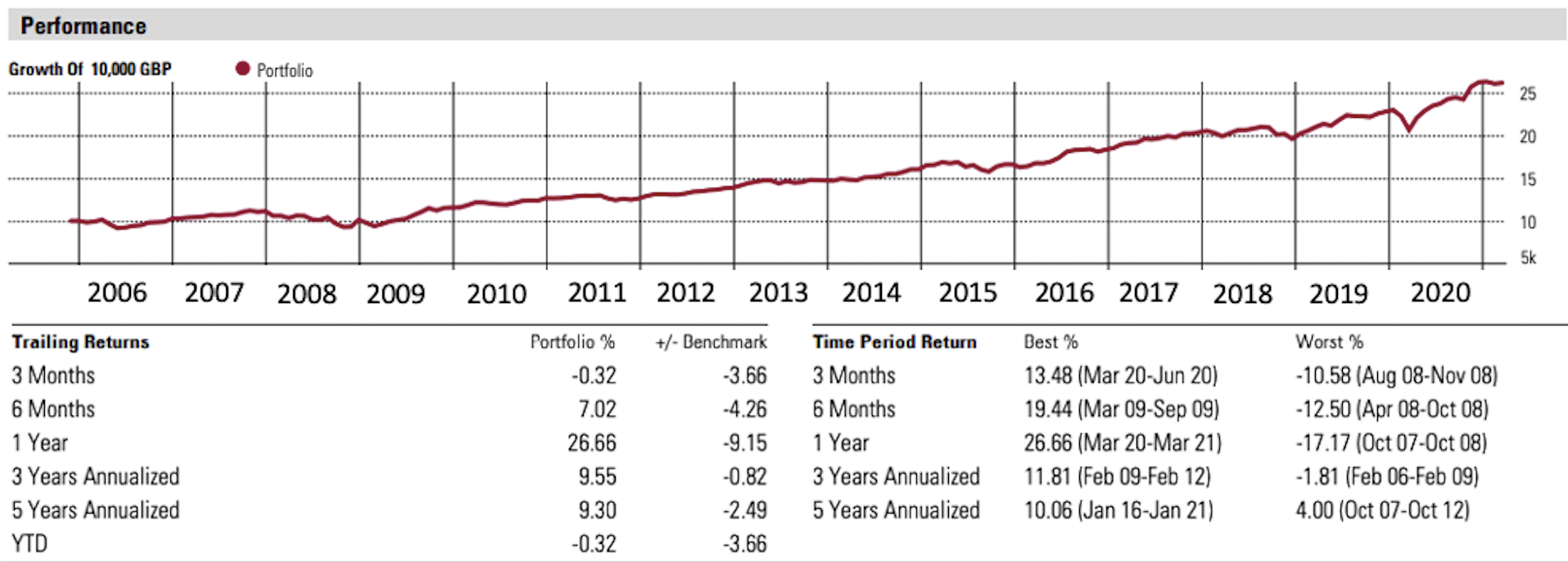

In the image below, I have shown the historic returns on a portfolio we recently designed for a client who has a low to medium attitude to risk. To ensure diversification, this portfolio was made up of 17 different funds from fund houses including Vanguard, Rathbones, Blackrock, Aegon, Fidelity, Baillie Gifford and several others (you can find out more about how we build client portfolios at www.chorusfinancial.es/investment-management). As an advisory firm who take a totally independent approach to fund selection, we are able to build our client portfolios from the leading fund houses in the world without any restrictions or bias, so the focus is always on value, experience and quality.

As you can see above, the performance data available for this portfolio goes all the way back to 2005. I like to ensure my clients receive comprehensive documentation and analysis for any portfolio I am recommending, including data that goes back as far as possible. We do always have to say, however, that past performance is no indication of future performance, and as I am about to confirm, portfolios can go down as well as up!

The analysis we provide when making a recommendation includes the last 5 year’s annualised returns, and in this example, investors would’ve seen an average 9.3% annual return before product and advice fees over each of the last 5 years. But what we also show are the worst and best historic returns for as far back as the data will take us.

Many of you will remember 2008 and it was certainly not a good year to be an investor! On the above portfolio, if you had held this portfolio from October 2007 until October 2008, your holdings would’ve fallen 17%! The 2020 Covid 19 drop last year was a mere blip, that recovered in a matter of weeks, compared to 2008!

However, what is reassuring, is that over the last 16 years, even if you had invested at the absolute worst time possible, from October 2007 to October 2012, you would still have seen an annualised return of 4%. So even considering that particularly awful year, you would have still come out on top if you had held for 5 full years.

A financial adviser can never truly predict the markets, but it is our job to ensure our clients understand risk, and we can help manage risk by keeping fees low, diversifying well and choosing quality funds for our portfolios. You should also never consider an investment or pension transfer unless you are willing to hold such a plan for a decent period of time. All historic investment data shows that one of your best friends when it comes to investing is time.

If you are considering financial advice on pensions or investments in Spain, Chorus Financial will happily provide a recommendation without any charge or obligation. We guarantee full fee transparency, coupled with qualified, regulated advice. Call Chorus today on +34 965 641 163, email [email protected] or visit www.chorusfinancial.es for more information.